Soviet Russia's Catastrophic Speed Run to Capitalism

Part I on the Operational Details of Russia's Transition to Capitalism

Part of a series on the operational details of Russia’s transition to capitalism

By the end of the 1980s, the Soviet Union saw the writing on the wall: their centrally planned command economy wasn’t working. Their people were poor, their supply chains were broken and rusty, and they struggled to compete in the global economy. They needed to evolve towards something more open and market-based. Their leaders didn’t know much about markets, no more than you might learn from reading a book. But they had built a near-religious belief that the solutions to their country’s many problems could be found at the intersection of supply and demand.1

Soviet leaders thought that transitioning the Russian economy to capitalism simply meant getting out of the way and letting the market do its thing. They had no idea that markets, especially national markets, are built up by over decades by millions of people performing millions of interconnected jobs. They had no idea that a market is an ecosystem whose balance is as complex and delicate as a rain forest’s. They had no idea that government doesn’t exist just to constrict business but also to enable it, to nurture it, and to protect it. So when Russia’s leaders finally did transition to capitalism, they birthed a market in crisis.

The Crime of Entrepreneurship

Let’s start with some background on the Soviet Union, a land before markets.

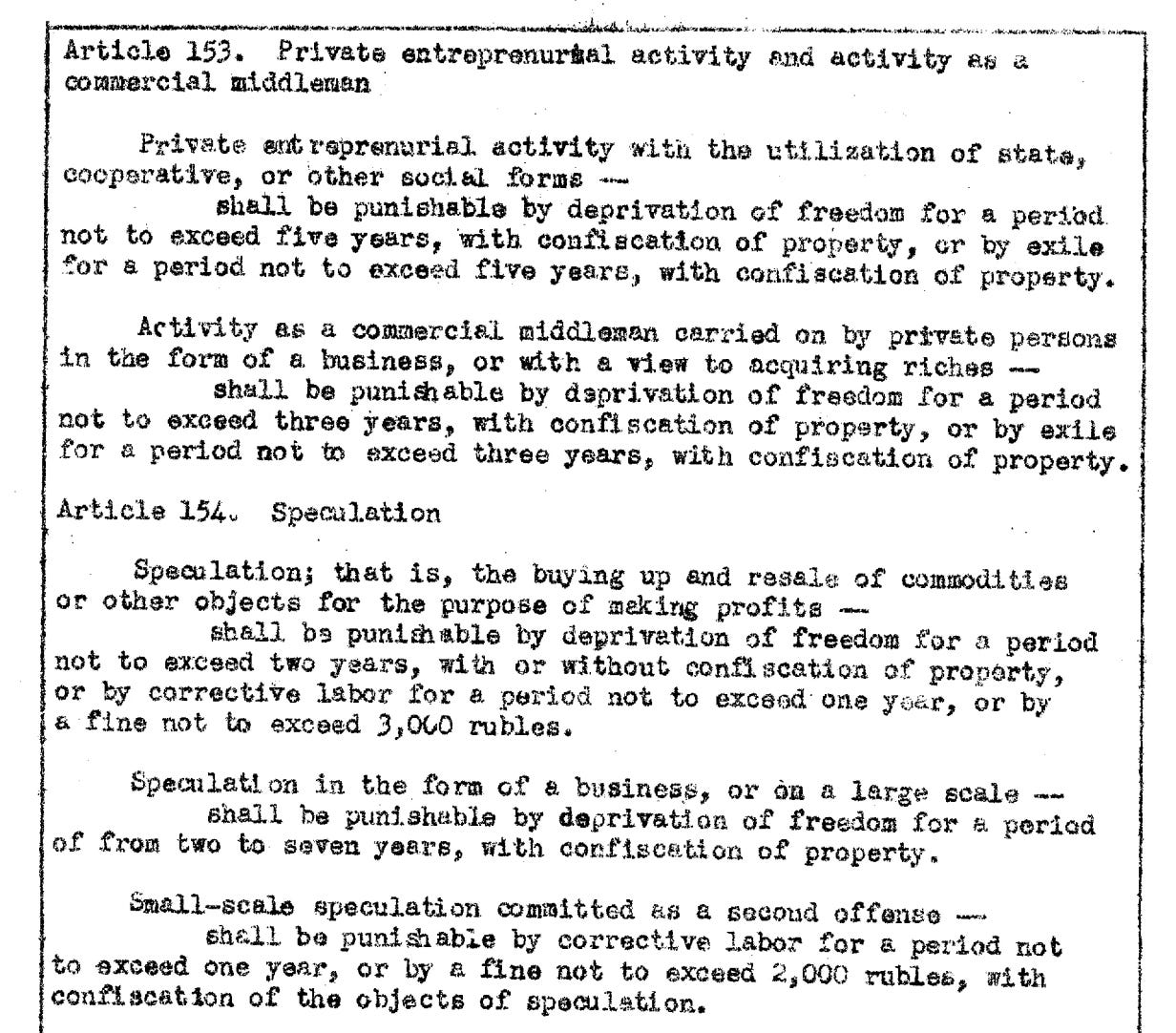

Soviet politicians and propaganda treated all entrepreneurship as profiteering. I’ll spare you from having to guess what the Soviets thought of any word whose root was “profit”: it was a crime.

Here are statutes outlining the punishments for the crime of entrepreneurship in the Soviet criminal code:

Okay, so markets are illegal, profits are illegal, and businesses are illegal. How did people in Russia get stuff they needed? Through state owned enterprises, whose outputs had been meticulously planned out years in advance. The people’s leaders had scheduled out the economy for everyone, and very much did not want their universe dented.

By the mid-1980s, it was abundantly clear that a centralized economy couldn’t give citizens what they needed. So the Soviets decided to reform it to be more open, under an agenda called glasnost. The agenda was made of many plans and laws, including the 1988 Law on Cooperatives, which made entrepreneurship legal for the first time.2 Immediately, street hawkers and small businesses - the microorganisms of a capitalist ecosystem - sprouted up in city centers across Russia.

Market opening reforms continued until 1990, when the Soviet economic agenda radicalized into a full-on transition to capitalism. So how, you may ask, did communist central planners expect to transform their economy into a free market? It turns out through a kind of central planning swan song - one final economic plan that would permanently lift price controls, legalize private property, and oversee the transition of nearly a million government enterprises into civilian hands.

That swan song was the 500 Days Plan, a top-down blueprint to speed run all of Russia into capitalism in, well, 500 days. I’m sure the 500 Days Plan was a glorious feat of bureaucratic poetry (no English version is available online). But any startup founder could have told Gorbachev that no matter how well-crafted your plan, it will fall apart upon contact with the market. Plans can only anticipate so much of what a market needs, because markets are made up of people, and people are complex, and complexity is unpredictable, especially when it’s aggregated.

Like Rome, a market economy is not built in a day. It builds up organically over decades of interaction between customers, talent, capital, and infrastructure. Compressing this timeline down to 500 days wasn’t just unrealistic. It was cruel. It was a disaster. It was Soviet planning’s final atrocity.3

You Can’t Just Learn How to Do Capitalism in 500 Days

Russian capitalism at its birth was everyone doing everything for the first time, at the same time, everywhere.4 This created a totally unique chaos: the chaos of a dysfunctional market, comprised of beginners in every station, with no sense of its own rhythm, and no stable prospects. That chaos is extremely challenging to describe when viewed from above.

That's probably why historians (especially academics with no commercial experience), discuss it so briefly. But if we view the chaos from the ground up, through the eyes of an Russian entrepreneur, we can see clearly both its shape and the burning need for order that it created.

The most immediate form of this chaos was the new strains of evil the market enabled. First, entrepreneurs found that success brought with it money, which in turn brought with it the attention of extortion-seeking thugs. Second, the markets were rife with fraudsters looking swindle honest businesses and promise breakers who had no scruples breaking a legally binding commitment.

For sure, beating and betrayal were traumatic experiences that left business owners feeling vulnerable. But the most important chaos came not from malice, but from novice incompetence. And that incompetence could be found at every layer of the market, starting at the very base.

Russian business owners had never managed cash before. The flow of cash in and out of company accounts is the beating heart of every well-run business. Cash flows in from your customers who pay the invoices you send them. Cash flows out from your bank account to pay the bills. The choreography of these tides is called cash flow management.

Like cooking, cash flow management is a simple skill that you can spend a lifetime mastering.5 When you do it right, the money from your sales comes in before your bills are due, so you don’t need to deplete your bank account to pay them. The money that's left over you can then reinvest into your business. This is the "capital" loop that comprises capitalism: you take the money you earn and you pour it back into your business to grow it further.

Also like cooking, cash flow management can be disastrous when screwed up. Either you are out of stock and waiting for customers to pay you before you can buy more, or your bank account is empty and your shelves are flush with stock that won’t move. In either case, your cash crunch can turn fatal if the patience of your vendors, employees, or landlord runs out before you have the cash to repay them.

This is why every business is rightly concerned about its cash flows. Many businesses, especially the ones that sell to other businesses—e.g. manufacturers and wholesalers—also must worry about the cash flows of their customers. Because if their customers cannot manage their cash flows properly, then there is a good chance that those customers will be unable to pay when their invoices are due.

On the day that the Supreme Soviet passed the Law on Cooperatives, the number of people in Russia who knew how to manage their cash rounded to zero. Same for the number of people who had collected an invoice from a customer. Remember, this activity was criminal and the vast majority of Soviet citizens did not want to know the real meaning behind the euphemism “a deprivation of freedom”.

So businesses, especially wholesalers, had to stake their own cash flows—the heartbeat of their companies—on the business management skills of customers who had literally never made a ruble before. Harrowing.

“No brainer!”, you might say, “Just require your customers to pay cash up front - problem solved, next question.”

If only it was that easy. There are many stripes of business, from grocers to pharmacies to wholesalers, that have to hold inventory for some time before they can sell it. Having worked in the supply chains of all three of these trades, I can tell you: the businesses you sell to don’t have cash to pay for the cooking oil, or the aspirin, or the bales of t-shirts that they purchase from you.

So if you sell to these types of customers, you can’t tell them to “sorry, cash only.” The very nature of their business means you have to provide them credit. As a result, all wholesalers and manufacturers have forced risk exposure to the cash management skills of their customers. If enough of your customers are in a cash pickle at the same time, their insolvency spreads upstream to you.

The only durable solution to this is widespread cash management expertise, so that everyone generally pays their invoices on time with cash generated from sales. But that would take years for Russian businesses to develop. What was the solution in the short term? Credit! Which brings us to the next problem…

Russian lenders had never managed credit risk before. In the first few years of the transition, thousands of private lenders and banks formed to dole out financing. If your business was tight on cash, it was often easier to get a new credit line than it was to chase down past-due invoices. And these institutions had healthy balance sheets: thanks to a near-operatic central banking crisis, Russia’s streets were flooded with capital looking for work.

Banks, totally new to the world of credit risk, disregard pesky best practices like “reserve requirements” that might tamper their growth rates. More importantly, lenders didn’t have much to work with when it came to underwriting their borrowers for creditworthiness.

First of all, there was no credit history to go off of. There were no credit reporting agencies in Russia (they didn’t pass a credit bureau law until 2004).6 Lenders most commonly use the credit scores of the owners of a business to extend it credit. This works particularly well for credit scoring small businesses which are commonly just a legal structure to house the direct work of the owners.

Second was the problem the very discipline of business accounting itself was still new to Russia, because who needed money counters back when money making was illegal? And if you, the lender, did receive financial statements, there was no way of verifying that they hadn’t been primped to tell a rosy story that wouldn’t be corroborated by, say, a visit to the business’s stock room.

Let’s take a step back and look at how this all works in a functional credit industry. Normally, when a lender starts up, its founders and management have done several stints previously in the credit departments of established financial institutions. They’ve been on teams that have managed the health of loan books for the long haul. They know, through years of hard-earned experience, how to judiciously expand the credit of their most trustworthy borrowers, and prune the credit lines of the less reliable ones.

In a well-functioning credit market, the market itself is a merit function as to whether a new lender gets to set up shop in the first place. This is because, after anything larger than an experimental loan book, lenders have to borrow the money they lend out from investors. That money comes from larger financial institutions—usually banks, union pensions, university endowment funds, or family offices (aka teams who manage money for extremely wealthy individuals). These establishments are notoriously skittish around credit risk because their mandates boil down to “don’t make number go down”.

They often require lenders to agree to restrictions on maximum and minimum loan size, the industry of borrowers, repayment periods, and more.

And oh, do they need data. They’ll demand snapshots of the loans you’ve originated, as well as your customer base (known in the industry as a “loan tape”, a carry-over phrase from the era when this data was stored on magnetic tape). They’ll want to see your loan originations, grouped by time cohorts, matched up with different versions of your underwriting model to assess how well your underwriting has improved with new loan performance data. They’ll demand fully fleshed out financials going back to the very beginning of your operation.

They’ll scrutinize all of this data closely. And finally they’ll scrutinize how effortlessly you’re able to produce this data. This is because lending is an operationally intensive business, and any lender who can’t pass an industry standard diligence process probably doesn’t have their act together enough to be entrusted with other people’s hard-earned money. If you can’t produce a detailed loan tape or itemized financials, how can I trust you to give out my money to thousands of customers and then get it back, with interest?

Their diligence is this thorough because the interest rate they charge you is lower than the interest rate that you charge your customers, leaving them less margin for error. Thanks to this emergent industry wisdom, the odds are slim that a new lender quickly goes bankrupt after opening its doors. And because all the other lenders in the industry had to go through this same vetting process, even if the new lender fails, the credit industry as a whole is probably still okay.

Russia’s credit system in the 90s was sort of like this picture of a healthy industry flipped on its head. No one had any experience yet, no one had any track record yet, no one had any data yet. So no one had any idea what they were doing yet.

A few borrowing cycles in, and businesses had maxed out their credit lines, oftentimes across multiple lenders. The lenders made the biggest rookie mistake in credit: it’s much easier to give out money than it is to get paid back. If the percentage of your loan book that is “non-performing” (i.e. loans that have been unpaid, for 90 days or more according to most lenders’ definition), exceeds the interest you charge on your loans, congratulations you’re officially losing money. And a lot of Russian lenders realized they were losing money.

Just a few years in, and the industry had its first ever credit bubble. The balance of Russia’s non-performing loans grew 5x from 1994-1996, when adjusted for inflation. Speaking of inflation…

Russian central bankers had never managed a currency before. Prior to 1992, the ruble that Russians had in their pockets was not a real currency as we understand it today. Yes, you could use it to purchase goods, but the “price” of those goods was not the result of supply and demand. Instead they were the rates set by central planners.

And the rubles that citizens used daily, the rubles people earned as wages, were not the same rubles that state enterprises used to do business with each other. The Soviets issued what may be the first purely virtual currency, the beznalichny (meaning “cashless”) ruble for these transactions. Beznalichny rubles weren’t “real”, in that there was no banknote representation of them and there was no way for state enterprises to use them to pay for their workers’ wages.

There was a separate “clearing” ruble that the Soviet Union issued to allow foreign businesses to get rubles to purchase goods exported by Soviet enterprises. The Soviet banking system had issued them as different banknotes, and set the exchange rate between the “clearing” ruble and the domestic ruble.

With a purchasing power determined by top-down bureaucrats, and firewalls to shield it from the gravitional forces of markets, the money in Russian pockets was less of a currency and more like arcade tickets that you could trade for prizes—I mean groceries.

So with the transition to capitalism, the ruble had to transform into a real currency. In July 1993 Russia re-monetized, meaning the central bank said “hey you have 60 days to trade your old Soviet rubles for the new Russian ones, after which they’ll be funny money”. From then on, the ruble’s strength determined by how well the Central Bank of Russia managed it, and the strength of the economy whose transactions it had the privilege to denominate.

Unfortunately, this process got off on the wrong foot. Due to aforementioned central banking drama (which we’ll discuss at a later date), the ruble devalued 785x from 1992-1994. To understand the very visceral impact this had on doing business, imagine yourself as a wholesaler of denim in Moscow.

You invoice a customer, one of the largest fashion outlets in Leningrad, for a purchase they make on credit. You give them 90 days to repay, known in industry jargon as “Net 90”. Giving a customer 90 day payment terms is fairly typical in the world of wholesale. What’s not typical at all is the invoice losing 85% of its value by the time it’s due, thanks to hyperinflation. But if you raised that invoice in 1992, a year when the ruble plummeted 26x, that’s exactly what would have happened.

Oftentimes, your customers would pay late even if you didn’t give them credit terms (because, remember, like you, they struggled with cash flow). When doing business in a hyperinflation economy, an invoice settled late is indistinguishable from theft. The customer gets the goods up front and by the time they pay, the money they hand over is worth a fraction of what it was when the transaction was booked. So in effect, they got stuff for free without your consent.

Can you see how all these pieces fit together to make it terrifying to trade? Nobody around you knows how to manage their cash, so your invoices never get paid on time. And while you try to collect those unpaid invoices, hyperinflation decimates their value. And even if you find a lender with a high enough blood alcohol content to finance you, that’s just kicking the powder keg down the road or onto someone else’s yard.

Survival in a market like this requires shorter time horizons and shrunken circles of trust. I’ve seen this very same dynamic play out first hand in my time having done business in the informal economy in Kenya, primarily with mom-and-pop corner stores and their suppliers, neither of whom can rely on the government to protect them or their business. In places where every company develops these survival instincts, they percolate into a culture that can make it frustratingly hard to do business.

Businesses had zero assurance besides their direct relationship with (and character assessment of) their counterparties that a transaction would clear. These pressures confined trade to Dunbar-scale webs, limited by person-to-person bonds. Everyday Russians, knowing that they had little other recourse, only dealt with proximate and familiar individuals - people whose collars they could grab should something go wrong.

This worked fine for the smallest businesses. But what about the businesses that didn’t want to stay small? Or those that could only work at a large scale, such as factories or wholesalers or refineries or mines? What about those who wanted to trade with businesses in other cities? Where—WHO—could they turn when there was no collar to grab?

It turned out that there was quite a bit of money to be made by anyone who could that question. And while there was much about the market that Russian leaders didn’t understand, they were spot-on about one very important fact: for every problem the market encounters, it will come up with a solution.

We’ll discuss that solution next time.

Bibliography & Further Reading

Cheryl W. Gray, Kathryn Hendley: “Developing Commercial Law in Transition Economies: Examples from Hungary and Russia.”

Vadim Radaev: “Russian Entrepreneurship and Violence in the Late 1990s.”

Vadim Volkov: Violent Entrepreneurs: The Use of Force in the Making of Russian Capitalism.

Svetlana Glinkina: “The Shadow Economy in Contemporary Russia.”

Juliet Ellen Johnson: “The Russian Banking System: Institutional Responses to the Market Transition.”

Boris Yelstin’s impromptu visit to a regional grocery store in Houston in 1989 moved him so deeply that, just a months before he would become Russia’s first post-Soviet president, he planned to found a regional grocery store chain in Russia as a solution to the country’s problems. He said: “I think we have committed a crime against our people by making their standard of living so incomparably lower than that of the Americans”.

What’s remarkable here is not just the economic shift, but the moral one as well. You can get a sense of how big of a turn this was from the choice of words. “Cooperatives” at the time were understood to be a Soviet wink-wink disguise for businesses. The Soviets knew this, but had to keep up the charade that they were communist.

This essay wouldn’t be complete without a call-out of China, who successfully transitioned from a planned to a market economy. Compressing what could fill several volumes in two paragraphs:

Under Deng Xiaoping, China gradually liberalized its economy over the course of nearly 25 years. It started with decollectivizing agriculture, which increased food output 25% from 1979-1984 (liberalization was “slow”, but results were undeniably fast). Then they moved to industrial output, allowing state enterprises to sell their surplus products on the open market. They allowed private businesses for the first time since Communists took over, and gradually their output overtook state enterprises. Finally, Deng’s government created Special Economic Zones, circumscribed trade zones in cities where businesses could trade with foreign firms without the bureaucratic overhead that came everywhere else. In case you hadn’t heard yet, China’s transition to capitalism was a smashing success.

It’s helpful to borrow from James C Scott, in Seeing Like a State, what describes as the Greek virtue of metis: “a wide array of practical skills and acquired intelligence in responding to a constantly changing natural and human environment.”

Metis was missing from the people inside the market, who had not yet built up the savvy to do business well. But it was also missing from the bureaucrats who thought something as complex as a market economy could be commanded into existence from above.

I know this after watching countless Kenyan retailers and wholesalers walk tight ropes, balancing heavy working capital with 3% net margins.